What is a good credit score?

Maintaining a good credit score is key to securing a financially healthy future. From access to better borrowing terms as well as more favourable buying and renting options, there are a variety of reasons why securing a good score should be a top priority.

But what is a good credit score - and what is a bad credit score, for that matter? And if your score is a little less-than-ideal, how can you boost it? Don’t worry, below we’ll outline the kinds of scores you should be aiming for, as well as how to improve your score if necessary.

What number is a good credit score?

Your credit score is like a financial footprint. It provides insight into your borrowing history and signals to lenders how reliable you are at managing your money. Factors such as late or missed payments, frequent credit card cash withdrawals, and having a joint account with someone who has poor credit can all affect your score.

Knowledge is key when it comes to your credit score. So, if you’ve got questions such as ‘What is a good credit score out of 1000?’ and ‘What is an excellent credit score in the UK?’ let’s dive into some figures.

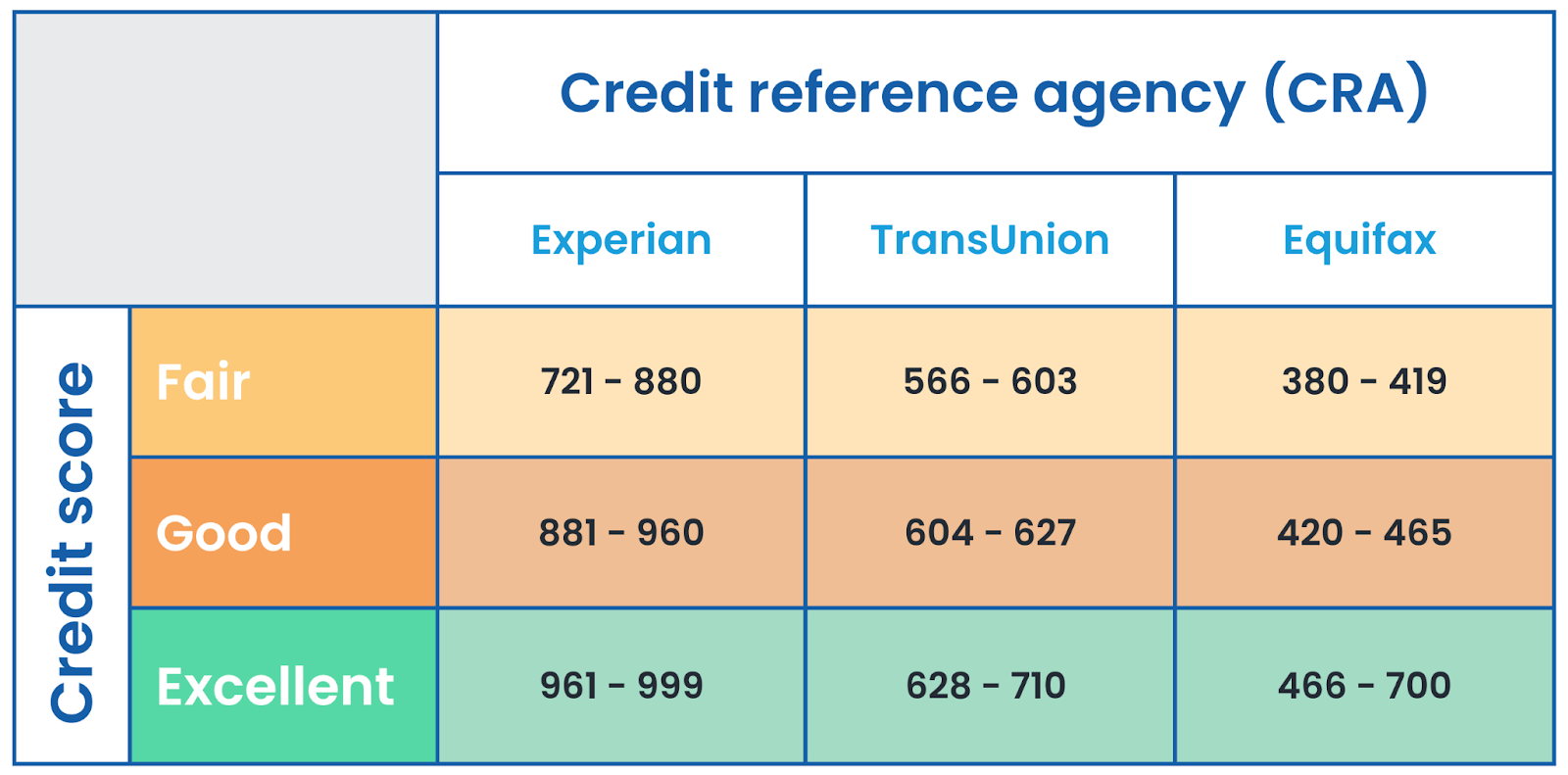

In the UK, there are three main credit reference agencies (CRAs): Experian, Equifax, and TransUnion. Each CRA uses a slightly different scoring system:

Experian: With Experian, a score of 721-880 is deemed fair, 881-960 is good, and 961-999 is excellent.

TransUnion: A score of 566-603 is fair, 604-627 is good, and 628-710 is excellent.

Equifax: A score of 380-419 is fair with Equifax, 420-465 is good, and 466-700 is excellent.

So, to answer the question: what is a good credit score number? The boundaries vary, but the higher the score, the more favourable you’ll appear to lenders.

How can I check my credit score for free?

The good news is that the process of checking your credit score for free is simple. By law, all CRAs will provide you with a free statutory copy of your credit report. If you want to see more detail, you can sign up for free trials with the CRAs to get a fuller version of your credit file - and there are also plenty of alternative options, too. Read our guide on how to check your credit score for free for all the details!

As always, if you do sign up to a service or create an account to check your credit score, make sure you check the terms and conditions with each of these services before proceeding.

The benefits of a good credit score

A good credit score could be the difference between securing an important loan for a car or a mortgage, or facing rejection. When you apply, lenders will contact their preferred CRA to assess your eligibility and flag any potential issues associated with lending to you. So the better your score, the better your chances of being accepted. Plus, you may have access to more competitive rates and favourable limits.

And remember, your credit score can also impact non-lending decisions, such as whether you’ll be accepted to rent an apartment. Also, in certain industries, employers review credit scores as part of the hiring process.

If your score is a little less than perfect but you need cash to help cover an unexpected expense, then a bad credit loan from Moneyboat could help. Even if you don’t have a ‘good’ credit score, or if you’ve been rejected for a loan in the past, we might be able to help. Just bear in mind that you’ll need to pass our affordability checks. As a responsible, fair lender, we have a duty to make sure you’re not borrowing more than you can comfortably pay back.

How to boost your credit score

So, if you’ve recently checked your credit score and it’s looking less than ideal, how can you go about boosting it? From practising responsible borrowing to limiting credit applications and remaining vigilant for errors, here are our top tips:

1. Don’t miss any payments

If you have existing debt, you’ll need to work towards steadily reducing it by staying on top of your repayment schedule. Late or missed payments can cause your credit score to dip significantly, with unpaid debts sometimes resulting in a County Court Judgment (CCJ) – something that can stay on your credit report for up to six years. So, to ensure all payments are made on time, we’d recommend setting up reminders or automatic payments in your banking app.

2. Keep credit utilisation low

Our next tip to boosting your score is keeping credit utilisation as low as possible.Your credit utilisation is the percentage of the credit limit you’re using. So, if you have a limit of £2000 and you’ve used £1000 of it, your credit utilisation will sit at 50%. The lower that percentage is, the more appealing you’ll look to lenders..

3. Limit applications

Making multiple applications for credit in a short space of time can signal to lenders that you’re in a hurry for credit. When you apply, a ‘hard search’ is usually carried out leaving a mark on your report. And while the impact of these can be short-lived, too many within a short space of time can build up, eventually lowering your score. We’d therefore recommend spacing out your applications, only applying for credit you’re confident you’ll be approved for.

4. Check for errors

It’s just as important to regularly monitor your credit report, checking for any inaccuracies or fraudulent activity that might have cropped up. Fraudsters might gain access to your details, using them to take out credit in your name. But if you regularly check your report, you’ll be able to identify any problems, quickly disputing them before they affect your score.

5. Build up a positive credit history

If you have little to no credit history, it can be difficult for CRAs to accurately score you. However, there are various steps you can take towards building a positive score, signalling to lenders that you’re able to responsibly manage your finances.

If you’re eligible to vote in the UK, start by ensuring you’re on the electoral roll by registering on the

GOV.UK website. Opening a bank account is another good step, and once you’ve demonstrated responsible account management, you may qualify for a credit card – something that when used responsibly, can be a huge help.

So, there we have it: our insights on what constitutes a good credit score as well as how you can work towards achieving one. While boosting your score won’t be instant, by paying off existing debt, disputing any inaccuracies, and limiting credit applications, you’ll soon see positive results.

And if you’re looking for more insights, you’ll find plenty over on the Moneyboat blog. There you can read our effective monthly budgeting tips as well as information on credit cards and bad credit and mortgages and bad credit.

Moneyboat are here to help

Here at Moneyboat, we offer support to customers across the credit spectrum. So, if you’re in need of funds to cover you until your next pay day, check out our flexible and fair short-term loans.

Looking at each application on a case-by-case basis, we carry out credit and affordability checks, assessing income and outgoings to ensure you’re a good fit. Providing affordable and responsible loan solutions, we’re committed to ensuring you can comfortably meet repayment deadlines and protect your credit score in the process.

Blog Disclaimer

We do all we can to bring you interesting, practical and valuable information. However, please understand the following:

- Moneyboat.co.uk are in no way connected or affiliated with the application or affiliate links mentioned in this or any article. We do not receive any commission and are not responsible for any charges that may result from any free trials or paid subscriptions.

- Moneyboat.co.uk does not provide medical advice It is intended for informational purposes only. It is not a substitute for professional medical advice, diagnosis or treatment. Never ignore professional medical advice in seeking treatment because of something you have read on the site. If you think you may have a medical emergency, seek medical advice immediately or dial 999.

- Information and data on this blog are for information purposes only. While we work hard to ensure it is accurate, we cannot accept responsibility for the accuracy, completeness, suitability or validity of any information provided on the blog. We will not be liable for any errors, omissions, losses, injuries or damages arising from its display or use. All information is provided with no warranties and confers no rights.

If you feel that any of the information published on our blog is not accurate, please notify us via email at thecrew@moneyboat.co.uk.

Representative Example: Borrow £400 for 4 months: 3 monthly repayments of £156.09 followed by a final repayment of £156.07. Total repayment £624.34. Interest rate p.a. (fixed) 288.35%. Representative APR 1,267.9%.

Compare Moneyboat loans.

Warning: Late repayments can cause you serious money problems. For help, go to www.moneyhelper.org.uk.

Latest blog posts

Explaining payday loan eligibility criteria

If you’d like to know more about eligibility criteria for payday loans, but don’t know where to start, you’ve come to the right place. We’ve put together a guide to help consumers navigate the choppy waters of the payday loans market.